So, you're thinking about healthcare, which means you're probably thinking about growing older, which might make you think about...well, a lot of things. But let's focus. One of the biggest questions looming for many approaching retirement is healthcare coverage. And in the swirling vortex of Medicare options, one name frequently pops up: AARP. Specifically, the AARP Medicare Supplement Plan G. But what exactly *is* it, and is it the right fit for you? Let's dive into the details, unraveling the complexities and exploring the ins and outs of this popular Medicare supplement plan.

Imagine Medicare as a giant puzzle. It covers a lot, but there are still gaps. These gaps, like the cost of copayments, coinsurance, and deductibles, can add up. That’s where Medicare Supplement insurance, often called Medigap, comes in. These plans, offered by private insurance companies like UnitedHealthcare (which partners with AARP), are designed to help fill those gaps, offering a safety net against potentially high out-of-pocket expenses.

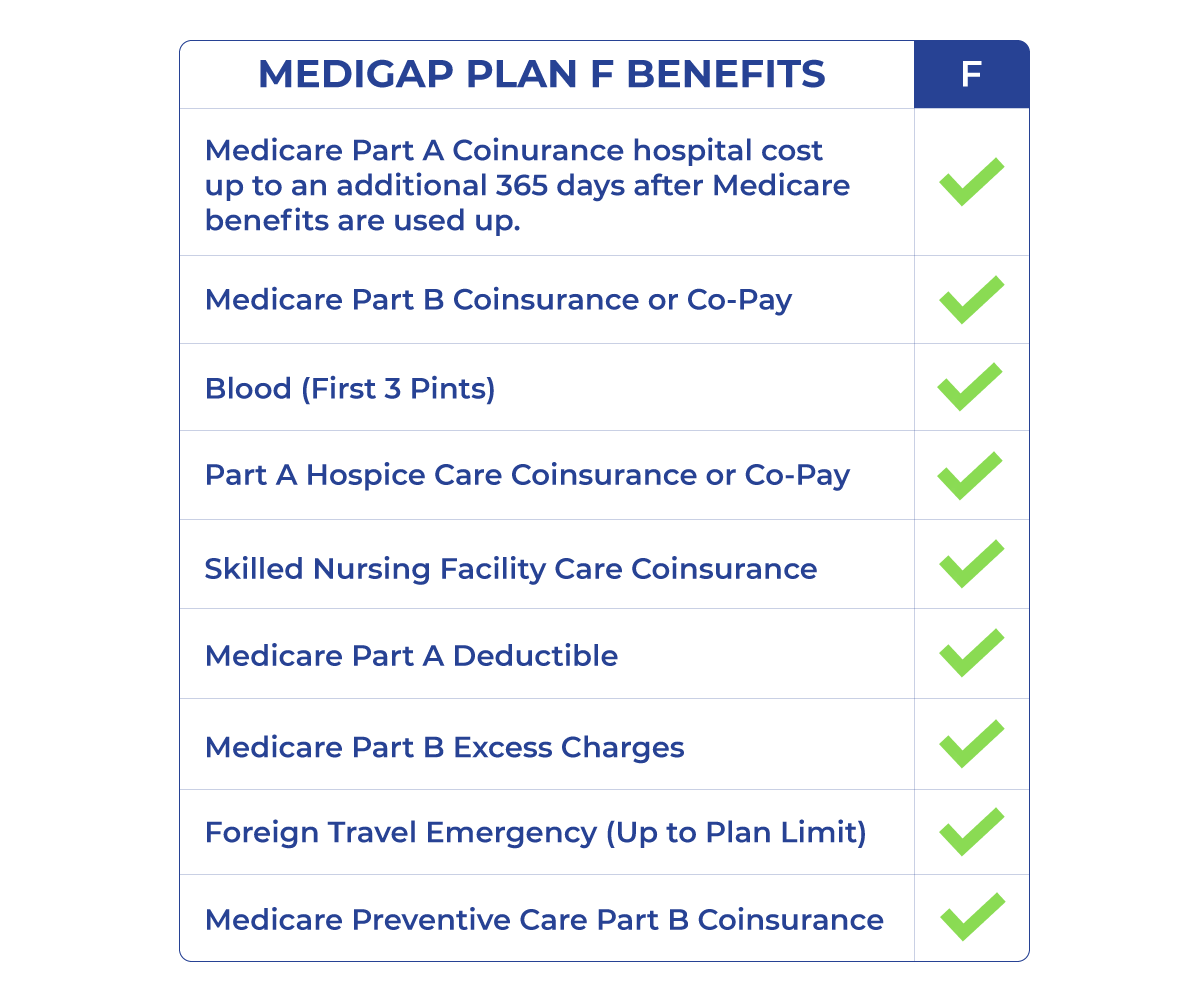

The AARP-branded Medigap Plan G is one of the most comprehensive options available. It covers a wide range of out-of-pocket costs, including Part A hospital coinsurance, Part B coinsurance and copayments, and even the Part A deductible. This can provide significant peace of mind, knowing you’re protected from many unexpected medical bills.

Now, here’s where things get slightly tricky. While AARP lends its name to these plans, it doesn’t actually *provide* the insurance. AARP partners with UnitedHealthcare, a leading insurance provider, which underwrites and administers the plans. So, when you see “AARP Medicare Supplement Plan G,” think “UnitedHealthcare’s Plan G, endorsed by AARP.” This partnership leverages AARP’s trusted reputation and UnitedHealthcare’s insurance expertise. But it's crucial to remember that the plan itself, including premiums and coverage details, is determined by UnitedHealthcare.

Before diving deeper, let's address a common misunderstanding. AARP Medicare Supplement Plan G is not the same as Medicare Advantage (Part C). Medicare Advantage plans are an *alternative* to Original Medicare (Parts A and B), often offering additional benefits like prescription drug coverage. Medigap plans, like Plan G, *supplement* Original Medicare, working alongside it to reduce your out-of-pocket expenses. You cannot have both a Medigap plan and a Medicare Advantage plan at the same time.

The history of Medicare Supplement insurance is intertwined with the evolution of Medicare itself. As Medicare evolved, gaps in coverage became apparent, leading to the development of Medigap plans to address these shortcomings. The standardization of these plans into lettered categories (like Plan G) further simplified the landscape for consumers. AARP's partnership with UnitedHealthcare to offer these plans became a significant factor in the market, making access to supplemental coverage more readily available to a large population.

One of the key benefits of AARP Medigap Plan G is predictable costs. While you pay a monthly premium, you'll have a clearer picture of your healthcare expenses, making budgeting easier. Another advantage is freedom of choice regarding doctors and hospitals. As long as they accept Medicare, they'll accept your Medigap plan. Finally, Plan G offers nationwide coverage, which is essential for those who travel frequently or split their time between multiple residences.

Advantages and Disadvantages of AARP Medicare Supplement Plan G

| Advantages | Disadvantages |

|---|---|

| Comprehensive coverage | Higher monthly premium compared to some other Medigap plans |

| Predictable out-of-pocket costs | Doesn't cover Part B deductible |

| Freedom to choose any Medicare-approved doctor or hospital | |

| Nationwide coverage |

Frequently Asked Questions:

1. What is the difference between AARP Medigap Plan G and Plan N? Plan G covers the Part B deductible, while Plan N does not.

2. How much does AARP Medigap Plan G cost? Premiums vary based on location, age, and other factors. Contact UnitedHealthcare for a personalized quote.

3. Can I switch from AARP Medigap Plan G to another plan? You may be able to switch during certain enrollment periods.

4. Does AARP Medigap Plan G cover prescription drugs? No, you'll need a separate Part D prescription drug plan.

5. Where can I get more information about AARP Medigap Plan G? Visit the UnitedHealthcare website or contact AARP directly.

6. Is AARP Medigap Plan G the same as Medicare Advantage? No, Medigap plans supplement Original Medicare, while Medicare Advantage is an alternative.

7. Who is eligible for AARP Medigap Plan G? Generally, those eligible for Medicare Part A and B are eligible for Medigap.

8. When can I enroll in AARP Medigap Plan G? The best time to enroll is during your Medigap Open Enrollment Period.

Choosing the right Medicare coverage is a crucial decision. AARP Medicare Supplement Plan G, offered through UnitedHealthcare, can be a valuable tool for managing healthcare costs and providing peace of mind. By understanding its benefits, limitations, and how it fits within the broader Medicare landscape, you can make an informed decision that aligns with your individual needs and financial situation. Explore the available options, compare plans, and don't hesitate to reach out to UnitedHealthcare or AARP directly for personalized guidance. Your future self will thank you for taking the time to navigate this complex yet critical aspect of retirement planning. Remember, securing your healthcare future is an investment in your overall well-being.

Unleash your inner artist mastering the scary clown drawing outline

Bmw i8 black edition electrifying darkness

Ending your elavon merchant services agreement